Long-term care insurance tax benefits sets the stage for this enthralling narrative, offering readers a glimpse into a story that is rich in detail and brimming with originality from the outset.

This type of insurance plays a crucial role in safeguarding your financial future, especially as you age. It not only covers various long-term care services, such as nursing homes and assisted living, but also provides significant tax advantages that can alleviate some of the financial burdens associated with long-term care planning. Understanding these benefits is essential for anyone looking to secure their health and finances in the years to come.

Understanding Long-term Care Insurance

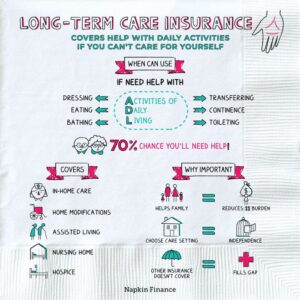

Long-term care insurance serves as a financial safety net for individuals requiring assistance with daily living activities over an extended period. As the population ages, the importance of securing this type of insurance continues to rise, ensuring that individuals can access necessary care without depleting their savings or burdening family members. This insurance can help cover the costs associated with various types of care, thus providing peace of mind to policyholders and their loved ones.Long-term care insurance primarily covers services designed to assist individuals who cannot perform basic daily tasks independently due to chronic illness, disability, or cognitive impairment.

It’s essential to understand the various types of services that are typically included in these insurance plans, as they can significantly impact the quality of care received.

Types of Long-term Care Services Covered

Long-term care insurance encompasses a variety of services tailored to meet the unique needs of policyholders. Understanding these services can help individuals make informed decisions when purchasing a policy. The main types of care covered include:

- In-home care: This includes assistance with daily living activities such as bathing, dressing, and meal preparation from trained caregivers in the comfort of the individual’s home.

- Assisted living facilities: These are residential communities that provide a level of support for individuals who need assistance with daily activities but do not require full medical care.

- Nursing home care: Skilled nursing facilities offer more extensive medical care and support for individuals with severe health conditions who require constant supervision and treatment.

- Adult day care: This service provides a structured environment for individuals needing supervision or assistance during the day, allowing caregivers a respite while ensuring care and social interaction for the individual.

- Respite care: Short-term care services that provide temporary relief for family caregivers, allowing them to take a break while ensuring their loved one receives necessary support.

Eligibility Criteria for Long-term Care Insurance Benefits

Eligibility for long-term care insurance benefits typically involves meeting specific criteria set by insurance providers. Understanding these criteria is crucial for individuals considering this insurance. Key factors include:

- Age: Most policies require applicants to be of a certain age, often between 40 and 85, to qualify for coverage.

- Health status: Insurers may require a health assessment to determine the applicant’s current health condition and any pre-existing conditions that could affect coverage.

- Functional limitations: To access benefits, individuals usually need to demonstrate an inability to perform a specified number of activities of daily living (ADLs), such as eating, bathing, and dressing.

- Waiting period: Many policies have a waiting period before benefits kick in, which can range from a few weeks to several months after the policyholder files a claim.

- Policy specifics: Each insurance policy may have unique requirements and limitations, which must be thoroughly understood to ensure adequate coverage.

Tax Benefits of Long-term Care Insurance

Long-term care insurance (LTCI) not only provides essential coverage for potential future care needs but also comes with several tax benefits that can significantly ease the financial burden on policyholders. Understanding these tax advantages is crucial for making informed decisions about healthcare planning and budgeting.One of the primary benefits revolves around tax deductions for premiums paid towards long-term care insurance.

Unlike many other types of insurance, the premiums for LTCI can be deducted from your taxable income, subject to certain limits. The amount you can deduct is based on your age and the total amount of your medical expenses. This tax deduction can help lower your taxable income, resulting in potential savings during tax season.

Specific Tax Deductions for Premiums

The IRS allows taxpayers to deduct long-term care insurance premiums as part of their medical expense deductions. The deductible amount varies with the age of the insured. Here’s a breakdown of the maximum allowable premiums that can be deducted for 2023:

- Age 40 or younger: $480

- Age 41 to 50: $890

- Age 51 to 60: $1,790

- Age 61 to 70: $4,770

- Age 71 and older: $5,960

To qualify for this deduction, your total medical expenses—including the deducted premiums—must exceed 7.5% of your adjusted gross income (AGI) for the year. This means that if you’re planning on purchasing LTCI, tracking these expenses can be beneficial come tax time.

Tax-Free Benefits for Qualified Services

When it comes to utilizing the benefits from your long-term care insurance policy, it’s important to note that the payouts for qualified long-term care services are often tax-free. This means that when you draw on your policy to pay for approved services such as in-home care or nursing home costs, you won’t owe taxes on those benefits. Qualified long-term care services must meet certain criteria set forth by the IRS, which generally include assistance with activities of daily living (ADLs) and care that is provided under a plan prescribed by a licensed health care professional.

These exemptions significantly increase the appeal of LTCI as a financial safeguard against the high costs associated with long-term care.

Comparative Tax Advantages with Other Insurance Products

Comparing the tax benefits of long-term care insurance with other insurance products reveals distinct advantages. For instance, while health insurance premiums can also be deductible, they do not offer the same level of tax-free benefits upon payout. In contrast, life insurance policies typically provide death benefits that are tax-free to beneficiaries but do not offer any deductions during the policyholder’s life.

This unique structure of LTCI makes it a powerful tool not only for care planning but also for tax efficiency. Here’s how LTCI stands relative to other insurance types:

| Insurance Type | Premium Deductibility | Tax-Free Benefits |

|---|---|---|

| Long-term Care Insurance | Yes, subject to limits | Yes, for qualified services |

| Health Insurance | Yes, generally | No, taxable benefits |

| Life Insurance | No | Yes, for beneficiaries |

Overall, the tax benefits associated with long-term care insurance make it a valuable consideration for individuals planning for their future care needs. With proper planning and understanding of the applicable tax laws, policyholders can maximize their financial benefits while ensuring access to necessary long-term care services.

Planning for Long-term Care

In today’s world, planning for long-term care is an essential part of securing a comfortable future. With an aging population and rising healthcare costs, it’s important to assess individual needs and explore available insurance options. This guide provides a structured approach for evaluating long-term care needs and integrating insurance into retirement strategies.Assessing long-term care needs involves understanding personal health conditions, family history, and potential future care requirements.

This process can help in determining the type and extent of coverage needed. Here’s a step-by-step guide to assist individuals in this assessment:

Step-by-Step Guide to Assess Long-term Care Needs

Understanding your long-term care requirements is crucial. This guide Artikels the key steps to effectively assess your needs:

- Evaluate Current Health Status: Consider any existing health issues that might impact your ability to perform daily activities.

- Review Family Medical History: Analyze your family’s health history for conditions that may require long-term care.

- Identify Daily Living Activities: List activities such as bathing, dressing, and eating to gauge potential assistance required.

- Consider Future Needs: Think about potential health changes as you age and how they might affect your care.

- Discuss with Family: Engage family members in conversations about care preferences and concerns.

- Consult Professionals: Seek advice from healthcare professionals or financial planners specializing in long-term care.

Evaluating long-term care insurance policies is a significant step in the planning process. The right policy can offer financial protection and peace of mind. Here’s a checklist to guide you through evaluating different policies:

Checklist for Evaluating Long-term Care Insurance Policies

This checklist will help ensure that you consider all important factors when reviewing long-term care insurance options:

- Understand Policy Types: Differentiate between traditional long-term care insurance and hybrid policies that combine life insurance.

- Check Coverage Details: Look for coverage of various care settings, including in-home care, assisted living, and nursing homes.

- Review Benefit Amounts: Assess daily or monthly benefit amounts to ensure they meet your potential care costs.

- Examine Waiting Periods: Understand the elimination period before benefits begin and how it fits your needs.

- Evaluate Premium Costs: Analyze premium affordability and potential increases over time.

- Consider Inflation Protection: Look for policies that offer inflation riders to keep up with rising care costs.

- Investigate Policy Exclusions: Familiarize yourself with what is not covered under the policy to avoid surprises.

Incorporating long-term care insurance into overall retirement planning is a strategic approach to ensure financial stability. Here are effective strategies for integrating this insurance into your retirement plans:

Strategies for Incorporating Long-term Care Insurance into Retirement Planning

Incorporating long-term care insurance into retirement strategies can provide a safety net. These strategies will help align your insurance with your overall retirement goals:

- Determine Appropriate Timeframe: Aim to purchase long-term care insurance in your 50s or early 60s to lower premiums and secure coverage.

- Budget for Premiums: Include long-term care insurance premiums in your retirement budget to manage costs effectively.

- Review Other Retirement Assets: Consider how long-term care insurance fits with savings, investments, and other assets.

- Prioritize Financial Goals: Ensure that long-term care planning aligns with other financial priorities, such as travel or inheritance goals.

- Adjust Plans as Needed: Regularly reevaluate your insurance needs and retirement plan as circumstances change.

Effective long-term care planning is a proactive approach that can safeguard your retirement and ensure peace of mind.

Closure

In summary, navigating the complexities of long-term care insurance tax benefits reveals a wealth of opportunities to protect both your health and your finances. By understanding how these benefits work and incorporating them into your overall retirement strategy, you can ensure a more comfortable and secure future. It’s never too early to start planning, so take the time to explore your options today.

Expert Answers

What are the tax deductions available for long-term care insurance premiums?

You may be able to deduct a portion of your long-term care insurance premiums based on your age and the limits set by the IRS.

Are long-term care benefits tax-free?

Yes, benefits received from long-term care insurance for qualified services are typically tax-free.

How does long-term care insurance compare to other insurance products for tax benefits?

Long-term care insurance often offers unique tax advantages that other insurance products, like health insurance, may not provide.

Can I use my HSA to pay for long-term care insurance premiums?

Generally, you can use funds from a Health Savings Account (HSA) to pay for long-term care insurance premiums, subject to certain limits.

Is there an age limit for tax deductions on long-term care insurance?

There is no specific age limit, but the amount you can deduct varies with your age, increasing as you get older.